How Can Small Businesses Manage Cash Flow Effectively And Avoid Pitfalls Of Small Business?

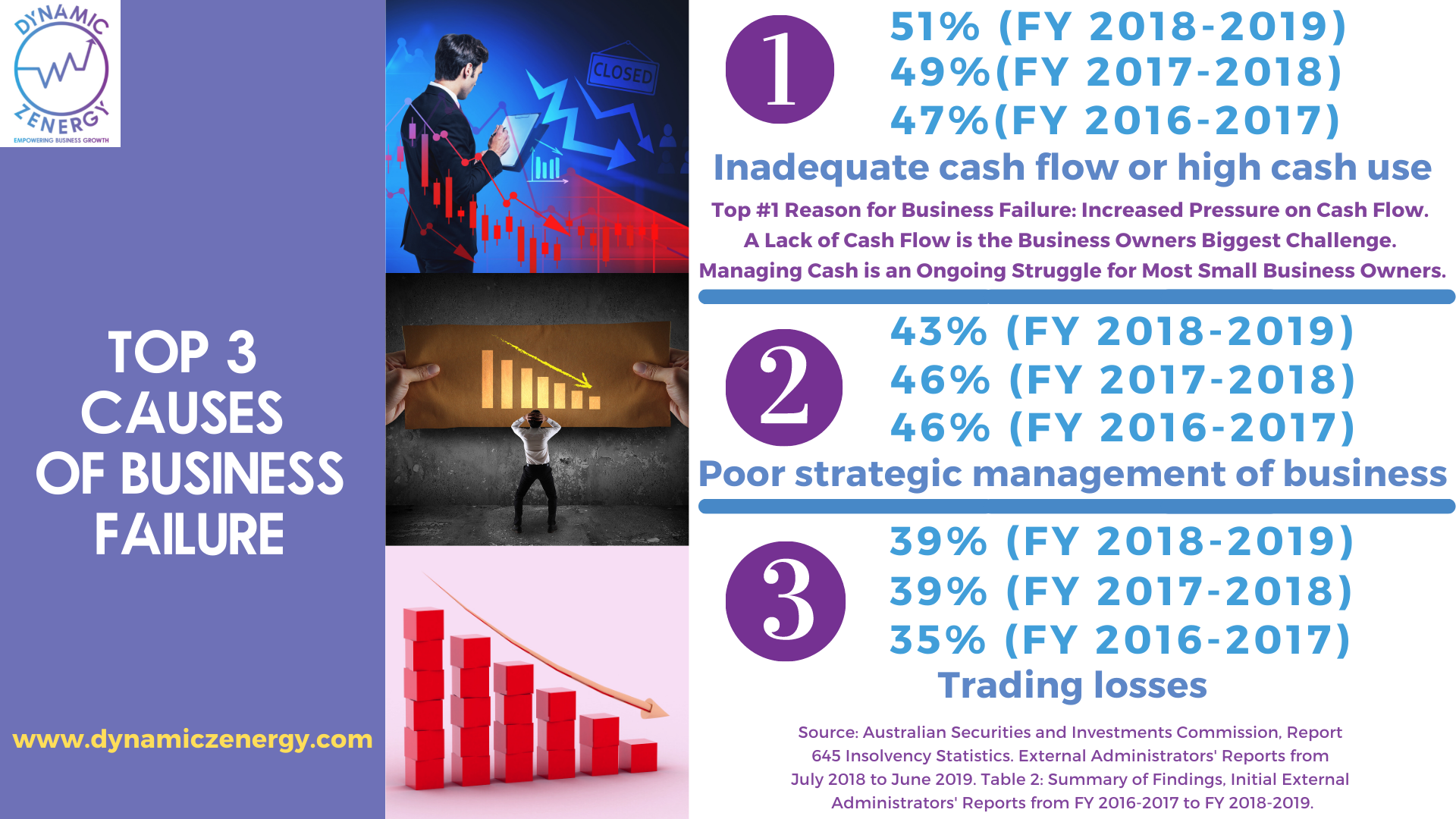

According to the Insolvency statistics report published by the Australian Securities & Investments Commission in December 2019, cash flow problems account for more than half of small business failures, making them the leading cause of business failure.

This article outlines how to prevent typical business cash flow challenges to accelerate your cash flow growth and manage your cash flow more successfully.

Clive Lewis, Head of Enterprise at the Institute of Chartered Accountants in England and Wales (ICAEW), emphasises that no business has failed due to a lack of profitability. However, numerous companies have failed due to a lack of cash, as cash is required for organisations to run.

Clive highlighted the importance of managing a company's cash resources and ensuring the organisation has enough cash to meet its needs and other financial obligations in the article he published.

What is Cash Flow in a Small Business?

Cash flow refers to the amount of money that enters and exits a small business account. Having a solid cash flow position is critical for small businesses to survive.

If your cash flow is insufficient where the organisation's expenses exceed the company's income, immediately address the cause of the financial health issues of the business. Positive cash flow does not always imply profitability. The revenue must exceed expenses for an organisation to be profitable.

Having positive cash flow does reflect the liquidity of the organisation. The benefits of having a high level of liquid assets in an organisation are as follow:

1. The more likely the organisation can obtain financing solutions.

2. The more likely the company can repay its short-term liabilities when it falls due.

3. The business is likely to meet its debt repayments.

4. The organisation can cope with unforeseen expenses such as unexpected market events or economic downturns.

5. It enables the company to reinvest funds back into the organisation.

6. The organisation can distribute profits to the business shareholders at a faster rate.

How Critical is Cash Flow to Small Businesses?

Positive cash flow enables you to expand your organisation through new ventures and personnel hiring. Negative cash flow indicates higher expenditure than income generated by the business, resulting in the company's failure.

Cash is the lifeblood of the business. Having a solid cash flow position enables the organisation to meet its obligations to pay for inventory, salaries, rent, and other operating expenses as it falls due.

If the business cash flow is suffering, get assistance in identifying the source of the problem, as this is the first step towards achieving a potential solution.

What are the Common Small Business Cash Flow Problems and How to Avoid Them?

Outlined below are strategies about cash flow management, from the basics of managing the business cash flow to tips on improving it.

1. Unknown Cause of Cash Flow Issues

Generally, determining that you have a cash flow problem is not straightforward. When spending surpasses available funds, it is self-evident that cash flow becomes an issue.

However, if you wish to address the cash flow issue, you must first identify the source of the problem. For many organisations, a cash shortage can occur without knowing the cause of the cash flow issue immediately.

Planning and organising the business financials are critical for better understanding the company's cash flow situation. Begin by categorising the business expenditures and recording the percentages associated with each expense category.

Suppose the current cash distribution makes no sense based on your company's business objectives and operations. In that case, there may be overspending in one or more expense categories. Prioritise spending reductions and modifications in high expense categories.

A financial professional, such as a part-time chief financial officer (CFO) or having an advisory board, can offer invaluable insight into your cash distribution. They may provide expert consultation on the current state of your cash flow distribution and make recommendations for improvement.

Hiring a part-time chief financial officer can improve the company's financial performance without committing to paying a salary of a full-time CFO.

2. Disorganised Bookkeeping Practices

Business owners are frequently overburdened, and bookkeeping often falls to the bottom of the priority list. Having disorganised books creates future headaches. If there are inconsistent invoicing, a lack of payment records and irregular billing of customers can result in loss of income and significant cash flow issues.

To stay on top of your business, consider hiring virtual assistants by using outsourcing services so you can focus more of your time on the areas that matter most in growing your business.

While organising your books takes time, it can aid in the identification of unpaid invoices and other errors that cost you money. Establishing an accounting system can assist in ensuring that your books are constantly up to date.

Using a business management system can generate financial and operational reports that provide insight into your company's performance. Suppose the staff lacks the talent required to maintain adequate accounting records. In that case, a part-time CFO may be a beneficial addition.

3. Not Using Cash Flow Benchmarking

The business' budget should be based on data to allocate funds to achieve the company's objectives. Suppose certain funds are allocated to business areas without any clear goal why spending in various categories occurs. In that case, it is risky and frequently results in cash flow problems.

It is all too easy to fall into a cycle of excessive spending, making subsequent reductions more difficult. Researching your industry and similar organisations' spending may assist in establishing a baseline for your cash position. To obtain the most realistic benchmarks, ensure that you select organisations in a similar lifecycle stage.

The scenario outlined above is another instance where the services of a financial professional or having an advisory board can be beneficial. Part-time chief financial officers can provide recommendations on improving and better managing your cash flow and assist in benchmarking your financial position.

4. Expenses are Excessive

Numerous businesses encounter this difficulty regularly. Expenses can quickly accumulate, frequently going unnoticed until a cash crunch occurs. Preventing the cash crunch is critical by conducting regular expenditure audits.

Recognise the expenses your business incurs consistently and identify which items might be reduced or renegotiated. Following your benchmarking exercise, you may discover that you are overspending compared to your competitors in the same industry. The benchmarking data may help renegotiate contract terms for large types of expenses.

5. Increasing Bad Debts

If a small business lacks a credit control system, bad debts can quickly accumulate. Cash flow challenges occur when the company cannot recover from customers the outstanding payments.

After you have structured your books and implemented an accounting system, the next logical step is implementing a credit control system. There are numerous methods for reducing bad debts, ranging from sending customers email reminders to partnering with a debt collection company.

6. Credit Terms are Inconsistent

Payment terms for your suppliers should be consistent with those for your customers. By synchronising your credit terms, you can improve your cash flow management. When credit conditions are out of sync, unanticipated spending can bankrupt or severely impact your cash flow.

If required, renegotiate agreements with suppliers and customers to bring your credit terms in line. Ensuring the payment terms for your suppliers and customers are consistent may be a significant and time-consuming project.

However, it will ultimately improve your business performance by balancing suppliers' payment terms with your customers to even out the company's cash flow.

7. Inventory Impacting Cash Flow

If your cash flow problems are not due to excessive spending, they may be due to your inventory or sales cycle. Maintaining inventory for an extended period ties up your assets, lowering your cash and storage space available.

It would be best to keep sufficient stock on hand to fulfil requests while holding inventory for the shortest possible time. It may even be essential to do a sales analysis to ascertain whether items or services have dwindling profit margins.

You can use your sales cycle to forecast your cash flow. Understand your sales cycle in detail to anticipate your inventory requirements and cash inflows effectively over time.

Additionally, it is critical to understand the seasonality of your sales cycle to plan accordingly. A part-time chief financial officer can aid with this effort by compiling several models and forecasts specific to your business and industry.

8. Unsustainable Growth Rate

While expanding your organisation is beneficial, uncontrolled business growth can result in cash flow issues. Expanding business activities may require hiring additional workers or increasing inventory, leaving you with unpaid wages and other expenses.

Uncontrolled expansion results in increased costs before receiving payment from customers. These cash flow issues can ultimately result in the company's failure.

If you are looking to expand your organisation, a financial advisor can provide invaluable guidance. Part-time CFOs can lead you through the process of growing your company at a steady rate that is sustainable over time.

How to Manage Small Business Cash Flow Effectively?

Cash flow management is critical to the success of any growing business. The following sections contain guidelines for small business owners on how to manage their cash flow.

1. Invoice Customers Promptly

Invoicing customers is an essential component of sound cash flow management. Do not wait to invoice after you have delivered a product or service. Delaying invoicing customers could be detrimental to the organisation's cash flow, impacting normal business operations.

Develop the process of promptly issuing customer invoices for payment. Consider invoicing promptly or frequently, depending on the nature of your business. If you are delivering a service, consider charging a deposit upfront or accepting payment in instalments.

The sooner you invoice the customer, the faster you receive payment. Billing customers is merely the beginning of managing business cash flow effectively. Maintaining good cash flow management requires strong income sources and collecting revenue from customers as soon as they fall due.

The invoice payment terms your organisation issues to customers can significantly impact the amount of cash brought into the business each month. By offering a 30-day payment term, you allow customers to pay after you have already provided them with the goods or services.

Suppose you anticipate increased cash flow requirements in the coming months. In that case, you may wish to alter your payment terms to guarantee funds reach your account more quickly.

2. Provide Electronic Payment Options

The customer can increase the company's cash flow position by accepting electronic payments to receive clients' payments more quickly. Provide customers with a simple and convenient method for paying invoices so that you increase the chance of receiving the amount soon.

Invoices sent via email and payment links included within the invoice might assist customers in streamlining the payment procedure. Consider offering loyal customers the option of automatic payments, guaranteeing that cash flows are coming into the organisation consistently each month.

3. Maintain Accurate Financial Records

Effective cash flow management relies on having good accounting and reporting processes in place. Prevent cash flow issues from getting out of control by ensuring that the accounting information is updated regularly in the accounting and business management system.

Implementing a good cash flow management process provides the ability to assess your company's financial health quickly at any time.

4. Forecasting Cash Flow

Cash flow forecasting is a proactive strategy for the organisation to prepare for potential financial difficulties. The cash flow forecast indicates the state of the company's financial situation for the next 30, 60 or 90 days.

Create a cash flow forecast regularly to determine the anticipated cash flow impact depending on the business cycle. Conducting cash flow forecasting is more important if the organisation experiences the seasonality of highs and low periods during the year.

Monitoring the organisation's cash flow position ensures the company can meet its financial obligations when they fall due. Performing cash flow forecasting increases awareness of what is heading your way, allowing the organisation to better prepare.

Cash flow forecasting allows the organisation to conserve part of its savings if the next month's cash flow is negative. It is essential to determine how to utilise best the periods of positive cash inflow to take advantage of ways to boost revenue.

5. Collect Receivables Promptly

Receivables are the amounts owing to your organisation, which are considered assets, often from clients who pay on credit. Accelerating accounts receivable to maximise cash flow is a critical technique to increase your company's cash on hand.

Calling in customer debt is one approach to increase the cash flow from assets in a month. Keep the communication direct and fair with customers when collecting outstanding payments.

However, do not be afraid to pursue a more official debt recovery process if necessary. Closely monitor the accounts receivable balance. If the accounts receivable balance is getting higher, increase your debt collection efforts.

The longer the outstanding invoices remain unpaid, the higher the risk that you cannot recover the debt, so act promptly to collect payments as soon as it becomes overdue.

6. Implement Stringent Credit Card Policies

Using company credit cards to make business transactions provide detailed tracking of the company's finances and the funds that leave your accounts each month. However, you must exercise caution in how you use and repay credit card debt.

Carrying a credit card balance over from month to month is not recommended, as it may result in further increasing your debt. Suppose it is challenging to minimise credit card use.

You may wish to lower the credit limit to avoid incurring more significant debt. However, before making any changes to the credit card limit, carefully review the company's credit card policy and the organisation's spending habits.

7. Maintain a Simple Bookkeeping System

If you lack confidence with numbers, consult a professional accountant. Utilise reputable accounting software to ensure that you are always aware of your current cash position. Having well-maintained financial records will assist in forecasting the company's cash flow for strategic business planning purposes.

For instance, suppose you anticipate a large order coming up next month, and you do not have up-to-date accounting records. In that case, it will be challenging to determine whether you have the working capital required to increase payroll or purchase additional inventory if needed.

When a significant opportunity presents itself, many small business owners are unprepared. Due to a cash shortage, some organisations cannot take advantage of good opportunities to increase revenue when the opportunity arises. Hence, the organisation should maintain a healthy business cash flow position.

Use a business management system that enables you to monitor and report on critical business key performance indicators (KPIs). These factors include the aging of receivables, operating profit margins, and inventory turnover.

A good understanding of the company's KPIs enables you to manage the business performance more effectively and implement strategies to take advantage of new market opportunities in growing the organisation.

8. Separate Business and Personal Finances

It is necessary to have a good process in place to track your business and personal finances separately. Having separate business and personal accounts provides a better understanding of the company's cash flow position.

It also allows conducting business forecasting much more straightforward to assess how the organisation's cash flow and performance might develop in the future. Combining business and personal finances can make it more challenging to determine how the organisation's performance is progressing towards achieving its objectives.

Separating the business and personal finances makes it easier to track how much income the organisation generates. It will enable you to assess how to compensate yourself appropriately and determine how much excess cash to reinvest in strengthening and growing the organisation.

9. Boost Revenue

While increasing cash on hand through higher sales may appear to be a simple task, it can be challenging due to fluctuating market changes and consumer demand.

Develop a strategy with the sales team to discover the quickest and most efficient way to get the products piling up as stock items into customers' hands.

10. Minimise Inventory

Eliminate or minimise inventory by quickly turning over the merchandise to ensure products get sold promptly, reducing inventory expenditures. Reduced inventory can help you save money on purchasing the products, delivery costs, and storage fees.

By stocking the minimum inventory level required, the business can keep its overhead costs low and improve its cash flow.

11. Establish Cash Reserve

The strength of the company's cash flow will determine the success or failure of the business. One of the critical strategies towards managing cash flow more effectively is to establish a cash reserve.

A cash reserve offers the buffer necessary to deal with unforeseen circumstances. It provides you with the confidence and funds required to expand your business.

Developing a sizeable cash reserve can be challenging. However, by doing so, the business can protect itself against the economic cycle. The organisation can also defend itself from the bank's decisions and other lenders, such as lenders increasing the interest rates of the business loan facility.

Additionally, it will enable you to capitalise on opportunities when they arise. For instance, you could buy inventory at a significant discount, take on a large order from a customer or secure a new client.

With a cash reserve, you can easily take advantage of different market opportunities to grow the business. Establishing a cash reserve puts you in a much stronger position. It may mean paying yourself less in the short term, but it will set your business on the path to success in the long run.

Maintaining a healthy cash flow is crucial for small businesses. Ensure you closely monitor the organisation's cash movements by using a business management system that allows you to track the company's financial performance regularly.

12. Securing Business Loans

Taking out a business loan can help enhance the company's cash flow. Obtaining a business loan entitles you to use other people's money to invest in your organisation. Loans are not included on your company's income statement because they are not considered revenue earned by the business.

Obtaining a bank loan can be a time-consuming process that involves credit checks and financial analysis. Some lenders provide businesses with immediate cash to get them out of a jam if you need short-term financing solutions.

If you believe a business loan is necessary, explore the small business loans available and merchant cash advance as alternative options from the traditional company financing solutions.

13. Lease Property and Equipment

Purchasing significant equipment or other assets necessary for the organisation's operations will negatively affect your cash flow. Typically, equipment and capital assets are expensive to buy, so you need to spend a sizeable portion of the company's revenue to cover the cost.

Leased assets reduce the constraints in the company's cash flow than ones purchased outright. If the business needs new equipment but lacks the cash flow to pay for it entirely, consider leasing or financing rather than buying the required equipment.

14. Discounts on Prices

Revenue generated from the sale of your company's products or services has the most significant impact on cash flow. A large inventory sale can provide a quick profit for the organisation while simultaneously lowering stock inventory.

The price reduction of an item may entice customers to acquire products they might not have purchased otherwise, resulting in increased revenue and cash on hand. When preparing for the following company's sale promotions, keep discount pricing strategies in mind.

15. Acquire Line of Credit

A line of credit can assist the business in navigating difficult times. A line of credit is distinct from a loan in that it is a revolving account, which allows a company to draw out the money, repay it, and then draw it out again.

By contrast, a loan is a one-time payment made to a business with strict repayment terms.

16. Cost Savings and Expense Tracking

One strategy for improving cash flow is to reduce the amount of money leaving the organisation at any given time. Monitoring the company's cash flow position involves eliminating non-essential expenses every month.

Keep track of the organisation's expenditure to determine the spending patterns in the company. If the business is experiencing a lean month when sales activities go down, examine the spending patterns and identify which expenses you can forego for the time being.

17. Delay Supplier Payments

Cash flow from assets and cash flow from current assets are intertwined. You invest money in inventory, and inventory has a monetary worth for your business. To carry a certain stock level, you must purchase products from suppliers, which results in a significant monthly cash outflow for the organisation.

If you need to enhance your cash flow in a given period quickly, speak with the suppliers to determine if they will allow payment deferral for specific invoices. However, be prepared to pay suppliers in full when the invoice due date occurs to avoid jeopardising the excellent relationship you built with them.

How Can Small Businesses Improve Cash Flow Fast?

The strategies outlined above can assist the organisation in increasing its cash flow. Using a business management system enables the organisation to make cash flow improvements more quickly and efficiently.

Implementing expense tracking procedures enables the organisation to gain control of the company's finances by monitoring funds that go in and out of your accounts each month.

Financial reporting and cash flow statements can assist the organisation in maintaining a pulse on the company's finances. Utilise a business management system to boost your cash flow immediately.

How to Easily Manage the Small Business Cash Flow?

The business must keep track of the funds going in and out of the organisation using a cash flow statement.

A cash flow statement is a critical component of financial management for the organisation. It allows for tracking the company's income easily and planning the organisation's expenses.

Utilise the cash flow statement template to assist with the company's payment planning process. Using the cash flow statement template helps ensure adequate funds are available to meet the organisation's financial obligations when they fall due.

How Can Small Business Benefit from a Cash Flow Statement?

A cash flow statement keeps track of all funds entering and leaving your business. It is beneficial to identify payment cycles or seasonal trends that indicate when the company requires additional cash to meet its financial obligations.

The cash flow statement can assist the organisation in planning and ensuring that the company always have adequate funds available to meet its financial obligations.

How to Create a Cash Flow Statement?

Enter the actual or projected values for the expense items each year. If you are utilising estimated costs, ensure they are appropriately labelled and justified.

Additionally, specify whether the figures are GST inclusive or exclusive on your cash flow statement. Outlined below are the different sections of the cash flow statement.

1. Opening balance

In the first month, specify the opening bank balance, and in subsequent months, it will be the closing balance from the previous month.

2. Incoming Cash

Incoming cash is the funds that are flowing into the organisation. If you are forecasting estimated figures, consider what forms of income the company may have and when you are likely to receive the funds.

Forecast when you are likely to receive the cash by assessing previous years financials. Identify if there are any seasonal trends and account for the sources of income the organisation receive regularly. The incoming funds for the organisation can relate to the following:

- Sales

- Debtors (a receipt of customer payments)

- Grants such as government grants received

- Tax rebates such as GST refund, income tax refund

3. Total Incoming Cash

Calculate the total incoming cash by adding together all the incoming cash items.

4. Outgoing Cash

The outgoing cash relates to expenses that the organisation pays. To forecast estimated figures, consider what costs the company expects to incur to operate the business and when the organisation is likely to settle the expenditure when it occurs.

Determine the pattern for outgoing cash by assessing previous years financials. Identify the periods for seasonal trends, if any and how the organisation will account for significant business expenses. The outgoing funds for the business can relate to the following:

- Accountant fees

- Advertising and marketing

- Purchases

- Rent and rates such as water rates and council rates

- Utilities such as electricity and gas

5. Total Outgoing Cash

Calculate the total outgoing expenses by adding together all the outgoing cash expenditure items.

6. Monthly Cash Balance

Calculate the monthly cash balance position for the organisation by subtracting the total outgoing cash from the total incoming cash.

7. Closing Balance

Calculate the closing balance position of the company by adding the opening balance and total incoming cash, then minus the total outgoing cash.

How to Develop Cash Flow Statement Fast?

Click on the button below to claim your FREE Done-For-You Cash Flow Statement Template to quickly create your company's current and forecast cash flow projections.

How to Organise Small Business Finances?

When starting or growing a small business, consider several factors regarding the organisation's financials, such as bookkeeping, processing business expenditure, and setting up a budget.

Outlined below are guidelines on keeping the company's funds organised to ensure the organisation's smooth operation.

1. Set Up Business Bank Account

Open a bank account for the business. However, according to the Australian Taxation Office (ATO), you are not legally required to establish a separate business bank account if you are a sole trader.

You can use your private or personal bank account for the business. However, it would help if you considered opening a separate business account to track your organisation's income and expenses easily.

According to the ATO, if you conduct business as a partnership, corporation, or trust, a separate business bank account is required for tax purposes.

2. Implement a Bookkeeping System

Organise the business finances by establishing a system for record-keeping purposes. Numerous manual and automated bookkeeping products may be appropriate for your organisation.

If you have hired a financial professional, speak with them about which products will work best with their systems. Establishing a basic bookkeeping system will help keep your company's books in order.

3. Creating a Budget

Creating a budget outlining the organisation's anticipated revenue and expenses will assist in managing the company's cash flow as you start and operate your business. Create the company budget as part of the organisation's strategic business planning process.

4. Payments and Invoicing Process

Decide on the company's payment terms and payment options that you can offer to customers. Create an invoice template and receipts to issue to customers when you sell products and services.

It is essential to provide a correct invoice to customers for the products and services you offer. Ensure the due date is specified clearly and follow up with customers immediately when they fall behind on their payments.

If the organisation provides subscriptions or memberships, consider establishing an automatic payment system. Consider setting a direct debit as a payment method you offer customers to avoid the hassle of chasing customers for their payments.

How to Analyse Small Business Finances?

Analyse the company's finances and track the organisation's performance to ensure the business maintains a healthy financial position.

Consider using a business management system to assist in automating the process of analysing the company's performance. The business management tool allows the business to proactively manage any potential financial risks and immediately address cash flow concerns as they occur.

Free Tools and Tips to Analyse Small Business Finances Easily

Monitor the business' health by utilising financial ratios to identify and resolve potential issues early on. Financial ratios differ between industries.

Comparing your company's financial ratios to a comparable industry's benchmark provides a reasonable assessment of how the organisation is performing.

Click here to discover more about the small business benchmarks that you can use to monitor the company's financial performance against the industry norms.

Business Health Check Calculators

Click here to access our FREE Business Health Check Calculators to help you stay on top of your business.

Business Viability Assessment

The business viability of a business refers to the state of an organisation's survival. The business survival is dependent upon the financial status and performance of the organisation.

According to the Australian Taxation Office (ATO), a business is viable if it satisfies one of the following conditions:

- It generates a significant profit to cover the business owner's expenses while also meeting its obligations to its creditors.

- It possesses adequate liquid assets that quickly turn into cash. Having liquid assets allows the organisation to sustain itself when the business is not profitable at a specific time due to its seasonality.

Business Viability Assessment Tool

Using the ATO's Business Viability Assessment Tool assist businesses in determining the long-term profitability of the organisation. The ATO requires you to submit several years worth of financial year's data to use the tool.

Click here to access the Business Viability Assessment Tool.

Use a Cash Management Solution to Achieve Profitability

Mike Michalowicz's book Profit First: Transform Your Business from a Cash-Eating Monster to a Money-Making Machine discusses the behavioural approach he developed. He turned the conventional accounting formula of Sales minus Expenses = Profit and changed the formula into Sales minus Profit = Expenses.

Mike demonstrates how business owners can change their organisations from cash-eating monsters to lucrative cash cows by prioritising profit first and allocating what remains for expenses.

By following four simple principles, you can simplify accounting for your business and make it easier to manage a profitable business by assessing bank account balances.

Organisations that reach early sustainable profitability increases their chance of achieving long-term business growth. The book provides a roadmap for business owners who wants to have a game-changing plan to achieve the financial success they have always desired.

Mike is one of the most innovative small business authors. He believes that profit is not an event. Profit is a habit. His Profit First technique is simple to implement and has a significant influence on the bottom line.

It can mean the difference between continually balancing on a financial tightrope and being consistently profitable. A predictable profit margin not only reduces stress and increases satisfaction, but it also enables you to focus on what matters, and that is, serving your customers.

Source: Amazon

Need Help to Boost Your Cash Flow or Profit?

Do you want to automate the cash flow management and strategic business planning process in your organisation?

When you systemise your organisation's cash flow monitoring and business planning processes, you can quickly assess how well you achieve your financial objectives.

Using a business management system, you can easily track the business financial performance progress against your company's strategic goals. The business management tool can assist in keeping you and your staff accountable to ensure you stay on track in accomplishing your organisational goals.

Disclaimer

This article does not constitute legal, business, financial, or accounting advice. All readers must seek the assistance of qualified professionals as required. When you use our affiliate link to purchase a product, we may receive a commission at no additional cost to you.| Tags:Business PlanningBusiness Finance |